Access Late-Stage Tech And Explore Investment Opportunities On EquityZen.

Explore our pre-IPO platform now.

Don't Miss This Post

A Co-Working Comparison: WeWork vs. IWG

When The We Company (formerly known as WeWork) filed its mandatory IPO paperwork last week, at least a part of us was hoping that the company’s disclosures would help rationalize its $47 billion private valuation. Instead, WeWork’s S-1 filing only helped to further reinforce what most of us already knew about the company: (1) rapid revenue expansion, (2) equally quick growth in losses, and (3) no path to profitability in sight. Moreover, I’m not sure the company’s disclosures did much to alter our understanding of WeWork’s status as a “tech company”—namely, that WeWork remains “not a tech company” but rather a co-working business with a serious maturity mismatch between its long-term lease obligations and short-term sub-leases.

"WeWork dismisses comparisons to IWG, instead calling itself a tech company. However, even when compared to recent tech IPOs with similar top-line metrics, its valuation remains a head scratcher."

- Phil Haslett, Chief Strategy Officer, Co-Founder of EquityZen

How Did WeWork Get Here?

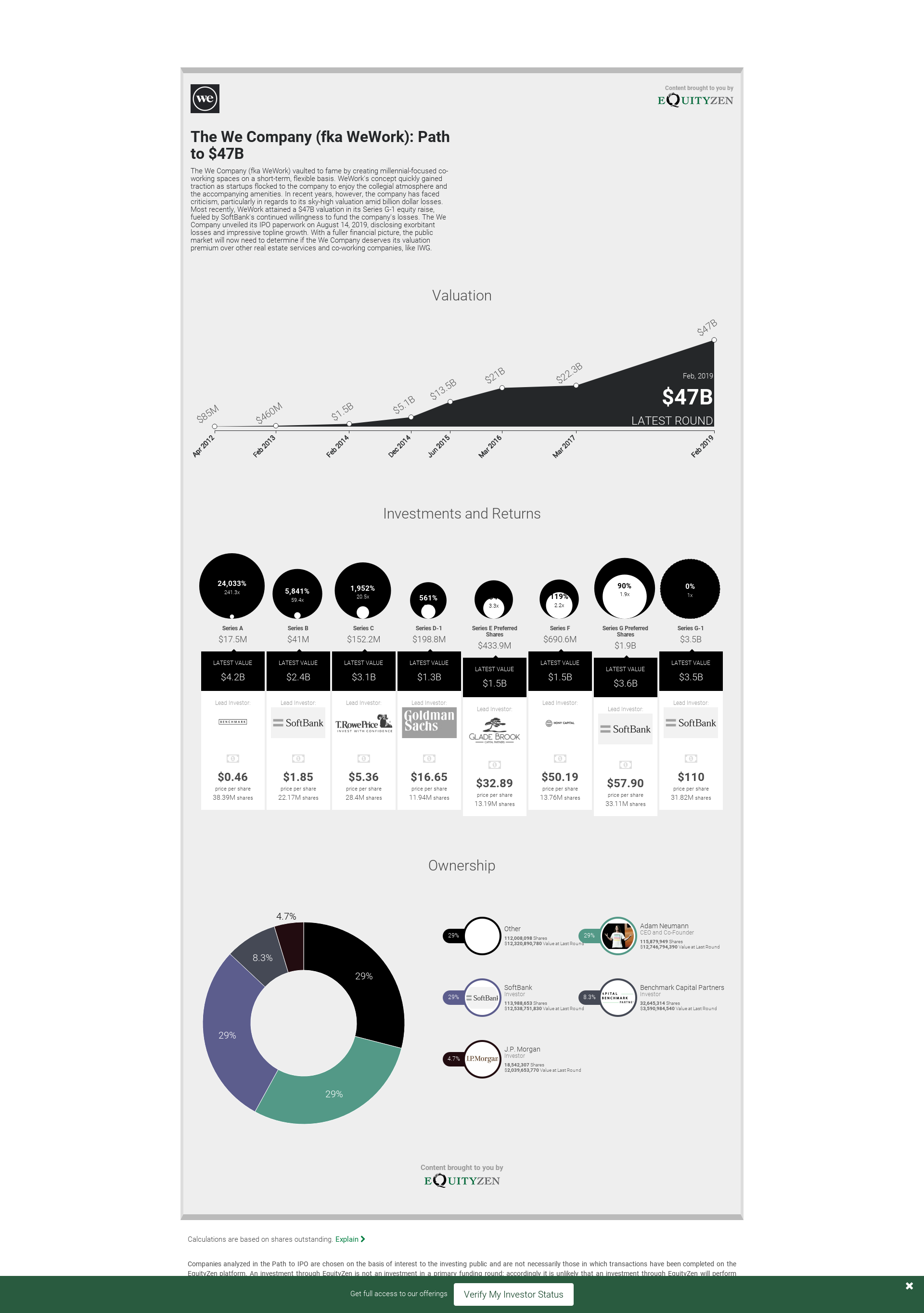

The We Company (fka WeWork): Path to $47B

The We Company (fka WeWork) vaulted to fame by creating millennial-focused co-working spaces on a short-term, flexible basis. WeWork's concept quickly gained traction as startups flocked to the company to enjoy the collegial atmosphere and the accompanying amenities. In recent years, however, the company has faced criticism, particularly in regards to its sky-high valuation amid billion dollar losses. Most recently, WeWork attained a $47B valuation in its Series G-1 equity raise, fueled by SoftBank's continued willingness to fund the company's losses. The We Company unveiled its IPO paperwork on August 14, 2019, disclosing exorbitant losses and impressive topline growth. With a fuller financial picture, the public market will now need to determine if the We Company deserves its valuation premium over other real estate services and co-working companies, like IWG.